Overview

With the final stages of the crop incoming, Mogiana region has had 20 days of good weather and don’t expect to see any huge drop in productivity compared to last crop. A 10-15% drop is mentioned as possible, besides more problems with aflatoxin compared to last year, all this due to the dry and high temperature periods in the early stages.

Recent reports from Alta Paulista show that the situation there has improved with the latest rains, the peanuts planted earlier will suffer more, but the ones delayed will not suffer so much.

December figures expose a considerable decrease in peanut exports, already expected as stocks grow shorter. Besides an 14% increase in oil exports.

Tables, charts and analyzes below:

Peanuts

Total

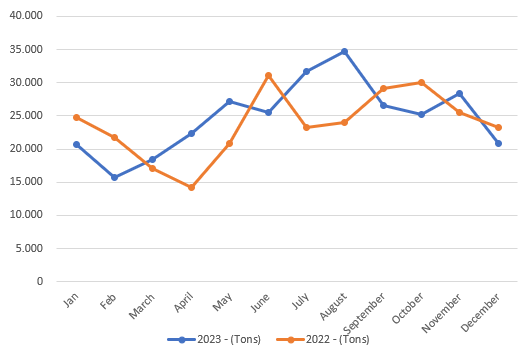

Peanuts export in 2023 x 2022

| Month | 2023 - (Tons) | 2022 - (Tons) | Var (%) |

|---|---|---|---|

| Jan | 20.702 | 24.698 | -16,18% |

| Feb | 15.756 | 21.798 | -27,72% |

| March | 18.472 | 17.132 | 7,82% |

| April | 22.425 | 14.161 | 58,36% |

| May | 27.193 | 20.885 | 30,20% |

| June | 25.542 | 31.055 | -17,75% |

| July | 31.630 | 23.327 | 35,59% |

| August | 34.730 | 24.030 | 44,53% |

| September | 26.620 | 29.200 | -8,84% |

| October | 25.150 | 30.057 | -16,33% |

| November | 28.339 | 25.576 | 10,80% |

| December | 20.889 | 23.324 | -10,44% |

| Total | 297.448 | 285.243 | 4,28% |

As usual, the final months of the crop will show a decrease in kernel exports, as the stocks from current crop decline, and exporters are focused on finishing their contracts and get ready for the new crop. December exports were of 20,9 thousand mt, 35% below November, and 10% below December 22.

With this addition, calendar year of 2023 is completed with 297,5 thousand metric tons exported, 4,28% more than 2022.

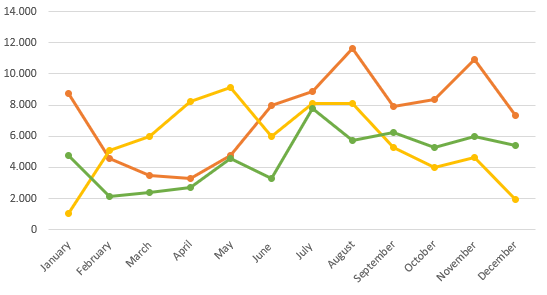

Destination

| Months | Russia | Algeria | EU27 |

|---|---|---|---|

| January | 8.754 | 1.077 | 4.758 |

| February | 4.594 | 5.065 | 2.118 |

| March | 3.473 | 6.000 | 2.385 |

| April | 3.300 | 8.215 | 2.686 |

| May | 4.781 | 9.123 | 4.549 |

| June | 7.965 | 5.973 | 3.320 |

| July | 8.865 | 8.077 | 7.777 |

| August | 11.630 | 8.132 | 5.761 |

| September | 7.900 | 5.290 | 6.250 |

| October | 8.333 | 4.025 | 5.271 |

| November | 10.935 | 4.625 | 6.013 |

| December | 7.364 | 1.925 | 5.403 |

| Total | 87.893 | 67.527 | 56.292 |

Russia and Algeria showed the biggest decreases, of 48% and 140%, respectively. EU dropped 11%.The exports going directly to Russia are the ones that showed a bigger increase, but Algeria and EU27 also increased.

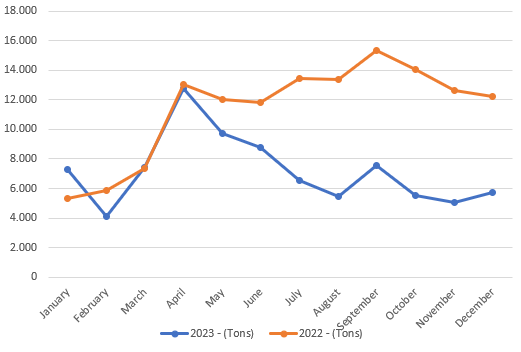

Peanut Oil

Peanut Oil export in 2023 x 2022

| Month | 2023 - (Tons) | 2022 - (Tons) | Var (%) |

|---|---|---|---|

| January | 7.298 | 5.301 | 37,68% |

| February | 4.092 | 5.852 | -30,08% |

| March | 7.439 | 7.359 | 1,08% |

| April | 12.746 | 13.023 | -2,12% |

| May | 9.706 | 12.045 | -19,42% |

| June | 8.807 | 11.836 | -25,59% |

| July | 6.543 | 13.446 | -51,34% |

| August | 5.456 | 13.364 | -59,17% |

| September | 7.555 | 15.370 | -50,85% |

| October | 5.544 | 14.023 | -60,46% |

| November | 5.062 | 12.625 | -59,90% |

| December | 5.763 | 12.211 | -52,80% |

| Total | 86.011 | 136.454 | -36,97% |

Oil exports have increased slightly, nevertheless are still very low compared to last year. Calendar year closes with 86 thousand mt exported, 37% less than 2022.

Destination

Exported volumes to main destinations so far:

| Month | China - MTs | Italy - MTs |

|---|---|---|

| Jan | 5.203 | 2.094 |

| Feb | 3.649 | 433 |

| Mar | 6.225 | 1.213 |

| Apr | 10.890 | 1.855 |

| May | 9.235 | 434 |

| Jun | 8.250 | 485 |

| Jul | 5.042 | 1.365 |

| Aug | 4.230 | 1.224 |

| Sep | 5.100 | 2.400 |

| Oct | 3.070 | 2.406 |

| Nov | 3.022 | 1.796 |

| Dec | 4.053 | 1.441 |

| Total | 67.969 | 17.145 |

On the oil side, China imported 1,000 MT more compared to last month, while Italy dropped 300 MT.