Overview

Planting for the 23/24 harvest is currently underway, with between 30 and 40% planted. The weather has been good so far, despite some late rain. Brazil appears to be dealing relatively well with delayed plantings, at least until November.

This development caused some concern among producers who held agricultural stocks, as a result of which prices fell slightly. Some shellers are purchasing farmer stocks to fulfill their contracts.

Peanut exports decreased and oil exports increased, compared to August figures.

With the presence of offers from China and India on the market, prices will fall, at least for now, mainly for Russia, Algeria and other “less strict” markets, when compared to the EU.

Peanuts

Total

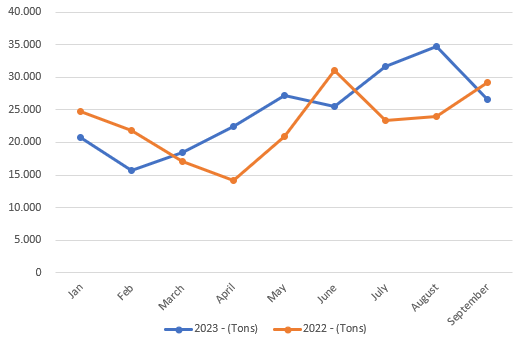

Peanuts export in 2023 x 2022

| Month | 2023 - (Tons) | 2022 - (Tons) | Var (%) |

|---|---|---|---|

| Jan | 20.702 | 24.698 | -16,18% |

| Feb | 15.756 | 21.798 | -27,72% |

| March | 18.472 | 17.132 | 7,82% |

| April | 22.425 | 14.161 | 58,36% |

| May | 27.193 | 20.885 | 30,20% |

| June | 25.542 | 31.055 | -17,75% |

| July | 31.630 | 23.327 | 35,59% |

| August | 34.730 | 24.030 | 44,53% |

| September | 26.620 | 29.200 | -8,84% |

| Total | 223.070 | 206.286 | 8,14% |

Peanut exports during September were 26,620 MTs, a decrease of 23% compared to August, and a decrease of 8,8% compared to September 22.

At the same time, during last year, we saw a peanut export increase, from 24,000 to 29,000.

Even so, this calendar year still adds up to 223,070 MT, an increase of 8.14% compared to last year.

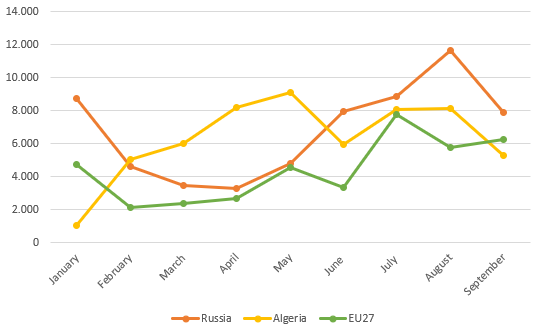

Destination

| Months | Russia | Algeria | EU27 |

|---|---|---|---|

| January | 8.754 | 1.077 | 4.758 |

| February | 4.594 | 5.065 | 2.118 |

| March | 3.473 | 6.000 | 2.385 |

| April | 3.300 | 8.215 | 2.686 |

| May | 4.781 | 9.123 | 4.549 |

| June | 7.965 | 5.973 | 3.320 |

| July | 8.865 | 8.077 | 7.777 |

| August | 11.630 | 8.132 | 5.761 |

| September | 7.900 | 5.290 | 6.250 |

| Total | 61.261 | 56.952 | 39.605 |

Exports to Russia went down 33%; to Algeria, a 35% decrease; and a slight increase of 8% to the EU.

This reflects the decrease in total exports, being Russia and Algeria the biggest importers so far.

Peanut oil

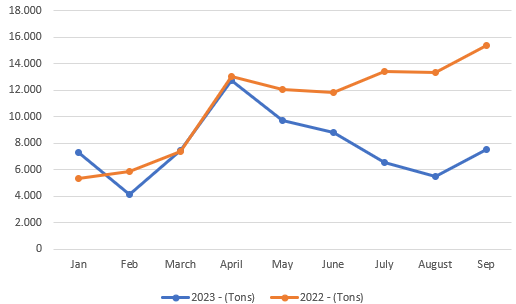

Peanut Oil export in 2023 x 2022

| Month | 2023 - (Tons) | 2022 - (Tons) | Var (%) |

|---|---|---|---|

| Jan | 7.298 | 5.301 | 37,68% |

| Feb | 4.092 | 5.852 | -30,08% |

| March | 7.439 | 7.359 | 1,08% |

| April | 12.746 | 13.023 | -2,12% |

| May | 9.706 | 12.045 | -19,42% |

| June | 8.807 | 11.836 | -25,59% |

| July | 6.543 | 13.446 | -51,34% |

| August | 5.456 | 13.364 | -59,17% |

| Sep | 7.555 | 15.370 | -50,85% |

| Total | 62.087 | 82.225 | -24,49% |

Oil exports increased 38% compared to August. But it's still a bad year compared to 2022.

Destinations

Exported volumes to main destinations so far

| Month | China - MTs | Italy - MTs |

|---|---|---|

| Jan | 5.203 | 2.094 |

| Feb | 3.649 | 433 |

| Mar | 6.225 | 1.213 |

| Apr | 10.890 | 1.855 |

| May | 9.235 | 434 |

| Jun | 8.250 | 485 |

| Jul | 5.042 | 1.365 |

| Aug | 4.230 | 1.224 |

| Sep | 5.100 | 2.400 |

| Total | 52.724 | 9.100 |